Pharmaceutical Solvents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.96 Billion |

| Market Size (2031) | USD 7.65 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Solvents Market Analysis by Mordor Intelligence

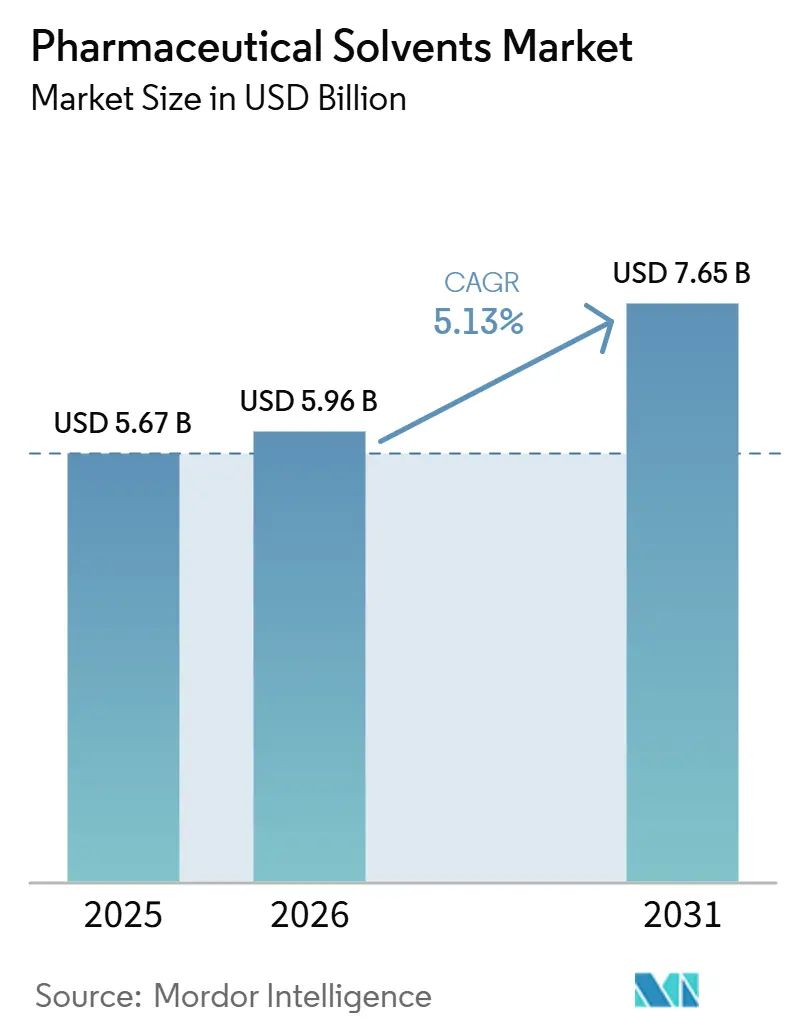

The Pharmaceutical Solvents Market size is expected to grow from USD 5.67 billion in 2025 to USD 5.96 billion in 2026 and is forecast to reach USD 7.65 billion by 2031 at 5.13% CAGR over 2026-2031. Recent growth reflects a decisive pivot by formulators toward ultra-high-purity grades that satisfy ICH Q3C and USP 467 residual-solvent limits. Alcohols, led by ethanol and isopropanol, command the largest share because they serve both synthesis and formulation steps. Demand is also rising for ionic liquids, supercritical fluids, and bio-based solvents as green-chemistry mandates spread. On the supply side, regional capacity additions in South Korea and the United States shorten lead times and insulate critical drugs from logistics shocks. Petro-feedstock volatility and stricter VOC (Volatile Organic Compounds) rules continue to favor suppliers that integrate recovery units and offer digital traceability.

Key Report Takeaways

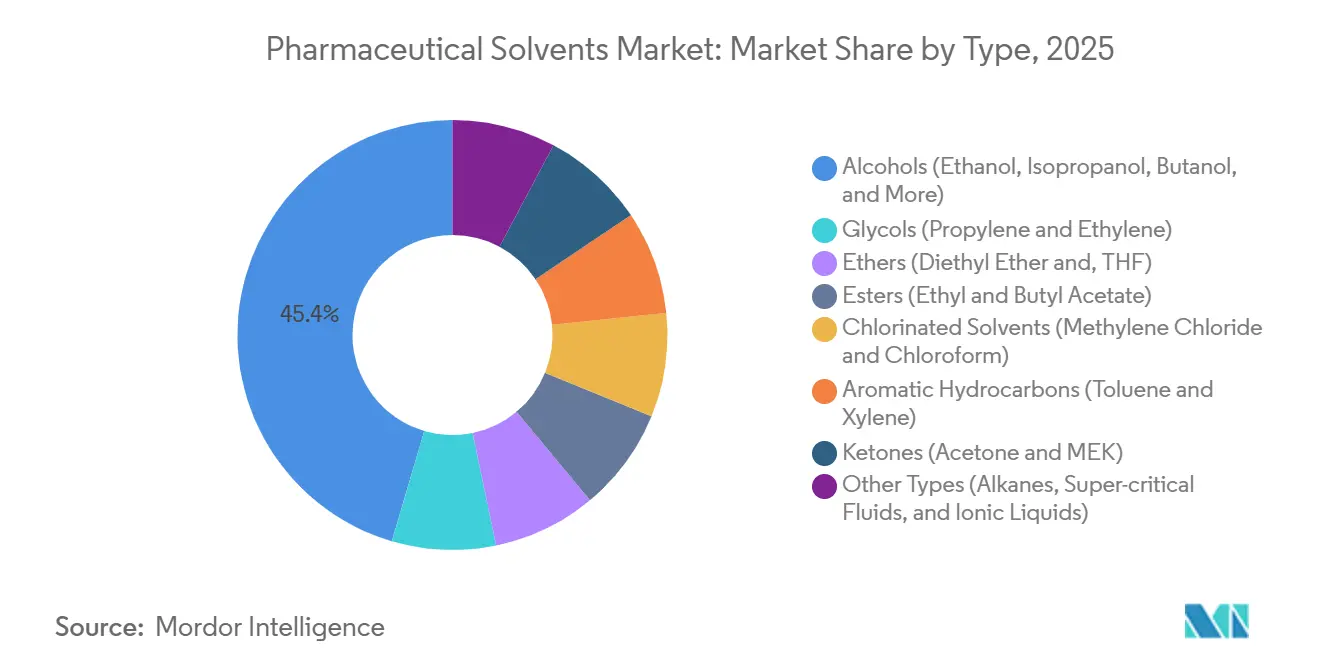

- By type, alcohols led with 45.45% revenue share in 2025; other types (alkanes, super-critical fluids, and ionic liquids) are forecast to expand at a 5.80% CAGR during the forecast period (2026-2031).

- By function, reaction-medium use held a 41.67% share of the pharmaceutical solvents market size in 2025; extraction solvent demand is rising at a 5.98% CAGR during the forecast period (2026-2031).

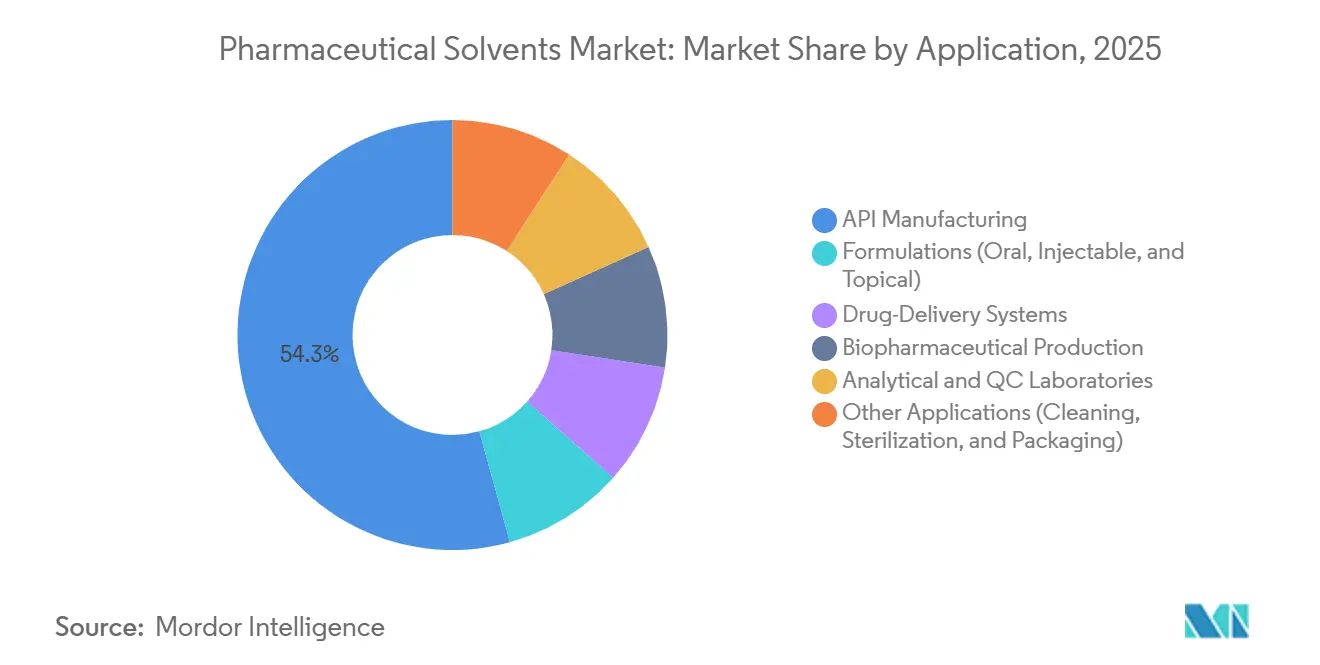

- By application, API manufacturing captured 54.30% of the pharmaceutical solvents market size in 2025, whereas biopharmaceutical production is projected to grow at a 6.23% CAGR during the forecast period (2026-2031).

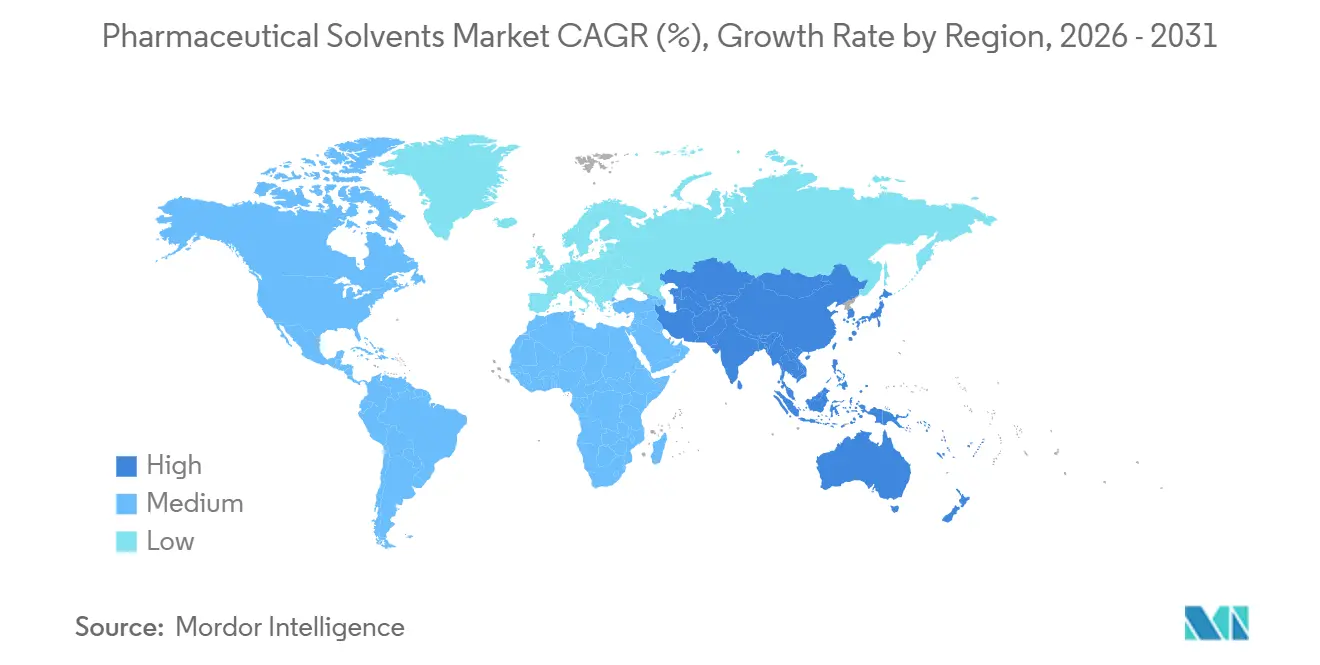

- By geography, Asia-Pacific accounted for 38.56% pharmaceutical solvents market share in 2025 while advancing at a 6.02% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Solvents Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing pharmaceutical production and R&D spending | +1.2% | Global, led by Asia-Pacific and North America | Medium term (2–4 years) |

| Increasing demand for ultra-high-purity solvents in biologics and HPAPI | +1.0% | North America, Europe, Asia-Pacific core | Long term (≥4 years) |

| Expanding generic and contract manufacturing capacity in emerging economies | +0.9% | Asia-Pacific (China, India), spill-over to ASEAN | Medium term (2–4 years) |

| Adoption of continuous-flow and solvent-recycling technologies | +0.7% | North America, Europe, select Asia sites | Long term (≥4 years) |

| Digital solvent-selection platforms shortening formulation cycles | +0.3% | Global, early adoption in North America & Europe | Short term (≤2 years) |

| Regulatory push for pharmacopeia-grade bio-based solvents | +0.4% | Europe (REACH, SSbD), North America (FDA/EPA) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Pharmaceutical Production and R&D Spending

Global drug output eased from 9.1% growth in 2025 to a still-solid 1.6% pace in 2026, yet biologics remain in double-digit expansion, lifting per-batch solvent intensity because monoclonal antibodies require multi-stage chromatography that consumes high-purity acetonitrile and methanol[1]Biopharma APAC, “Global Biologics Growth Outlook,” biopharma-apac.com. Asia’s share of Phase III trials now exceeds one-third of global totals, steering incremental solvent orders toward Chinese and Indian suppliers that have upgraded fractional-distillation lines to pharmacopeia standards.

Increasing Demand for Ultra-High-Purity Solvents in Biologics and HPAPI Manufacturing

Biologics fill-finish suites specify low-endotoxin grades, and closed-system transfers eliminate opportunities for on-site recovery. Merck’s EUR 300 million (USD 346.5 million) bioprocessing hub in Daejeon is positioned to supply just-in-time volumes of sterile THF and dimethylformamide to vaccine makers.

Expanding Generic and Contract Manufacturing Capacity in Emerging Economies

India operates more than 750 FDA (Food and Drug Administration)-approved plants, while China’s CDMOs keep winning multi-year supply contracts for novel drugs destined for Western markets. Each new reactor train raises solvent throughput, yet many local producers still import USP-grade ethanol, maintaining opportunities for global suppliers of specialty grades.

Adoption of Continuous-Flow and Solvent-Recycling Technologies

Eli Lilly reports 30-50% cuts in solvent use after shifting select APIs to continuous-flow systems. Meanwhile, distillation skids that reclaim up to 95% of spent isopropanol are becoming standard in greenfield biologics plants, driven by EPA (Environmental Protection Agency) air-quality permits that cap VOC emissions[2]Environmental Protection Agency, “VOC Standards for Pharmaceuticals,” epa.gov.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and residual-solvent regulations | -0.60% | Global, strictest in Europe and North America | Medium term (2–4 years) |

| Petro-feedstock price volatility | -0.50% | Global, acute in import-dependent regions | Short term (≤2 years) |

| Rise of solvent-free/solid-state synthesis routes | -0.40% | North America & Europe, pilot adoption in Asia-Pacific | Long term (≥4 years) |

| High capex for on-site GMP solvent recovery systems | -0.30% | Global, most acute for small-to-mid CDMOs in emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Residual-Solvent Regulations

ICH Q3C and USP 467 impose ppm-level caps on residual solvents, forcing reformulation away from methylene chloride and chloroform. Europe’s REACH fees reach EUR 500,000 (USD 575,930) per substance and are nudging formulators toward lower-toxicity esters and bio-alcohols.

Petro-Feedstock Price Volatility

Brent crude fell from USD 75.93 per barrel in January 2025 to USD 64.88 in April 2025, lifting acetone and IPA price spreads and squeezing generic-drug margins. Integrated suppliers hedge with vertical feedstock positions, but many mid-tier processors pass through surcharges to CDMO (Contract Development and Manufacturing Organization) customers.

Segment Analysis

By Type: Alcohols Anchor Volume, Next-Generation Solvents Gain Traction

Alcohols held 45.45% of 2025 revenue. Within the pharmaceutical solvents market size, isopropanol consumption alone topped multiple million metric tons, propelled by sanitizer, API, and lyophilization demand. Glycols and ethers fill niche roles but face toxicity scrutiny, while chlorinated solvents keep retreating under regulatory pressure. Other Types, ionic liquids, supercritical CO₂, bio-based alcohols, are on a 5.80% CAGR trajectory, reflecting green-chemistry incentives and continuous-flow compatibility. Despite limited installed capacity, early adopters value the improved selectivity and lower VOC profile that these alternatives deliver, positioning them as strategic growth nodes in the pharmaceutical solvents market.

The competitive response centers on capacity upgrades to handle pharmacopeia-grade purification. BASF’s 290,000 tons per annum THF Pharma complex is now paired with a Michigan GMP (Good Manufacturing Practice) Solution Center that offers on-site blending support. Japanese producers focus on renewable feedstocks; Mitsui’s bio-isopropanol plant underscores a move toward circular-carbon products. As supply chains diversify, traditional aromatics lose share, a trend amplified by tariffs that erode export economics into key demand centers.

Note: Segment shares of all individual segments available upon report purchase

By Function: Reaction Medium Dominates, Extraction Accelerates

Reaction medium use represented 41.67% of the 2025 value in the pharmaceutical solvents market share tally, largely because nearly every step of API synthesis depends on solvent polarity to steer kinetics and heat management. Continuous-flow reactors tighten specifications further, favoring low-viscosity, narrow-boiling-range grades that minimize fouling. Extraction solvents will post the fastest 5.98% CAGR through 2031. Biologics facilities rely on multistage liquid-liquid extraction and chromatography, each stage consuming high-purity acetonitrile or methanol. Suppliers respond by bundling solvents with resins and columns, turning what was once a commodity buy into an integrated process solution.

Formulation and blending remain mature but stable, as digital solvent-selection tools improve first-pass success rates and limit costly late-stage process changes. Analytical-grade demand rises in tandem with ultrahigh-performance chromatography, which mandates parts-per-billion particulate thresholds. Cleaning and sterilization keep their volume anchor status, yet stricter VOC rules will accelerate closed-loop recovery system adoption, reinforcing the sustainability narrative.

By Application: API Manufacturing Leads, Biopharma Surges

API manufacturing accounted for 54.30% of 2025 revenue in the pharmaceutical solvents market. Producing 1 kg of API can create up to 180 kg of solvent waste, so recycling infrastructure now accompanies most new reactor trains. Formulation work follows in scale but grows more slowly, constrained by generic-drug margin compression. Drug-delivery systems, liposomes, and nanoparticles demand specialty solvents to dissolve hydrophobic payloads, nudging dimethyl sulfoxide and N-methylpyrrolidone into higher-value niches.

Biopharmaceutical production stands out with a 6.23% CAGR through 2031, outpacing all other applications. Each liter of added mammalian-cell capacity in Samsung Biologics’ new Songdo campus will translate into kilograms of high-purity extraction solvents. Analytical and QC labs secure steady, high-margin demand backed by the broader reagents market’s growth profile. Cleaning, sterilization, and packaging cover the residual share and serve as stable baseload volumes.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific captured 38.56% of 2025 revenue and is forecast to grow at 6.02% CAGR through 2031. Chinese CDMOs keep adding stainless-steel fermenters, while India’s FDA-approved sites exceed 750, securing a floor for commodity alcohol consumption. South Korea’s USD 4.8 billion third bio-campus further tightens downstream demand for USP-grade THF and acetonitrile. A two-tier supply structure is emerging: multinationals import ultra-high-purity grades, whereas domestic generic firms buy competitively priced local alcohols.

North America ranks second. U.S. consumption of USP-grade isopropanol topped 870,000 tons last year, and BASF’s Michigan GMP center plus ExxonMobil’s Louisiana expansion demonstrate a clear localization push. Foreign investors like Celltrion are acquiring U.S. plants to navigate tariff complexity, ensuring solvent off-take stays domestic.

Europe’s share is pressured by energy prices and REACH fees, yet the bloc remains a specialist hub for high-value APIs. Dow, LyondellBasell, and Sabic closed crackers, tightening olefin supply. Survivors such as INEOS now market low-VOC, pharmaceutical-grade isopropanol aligned with the EU Safe and Sustainable by Design program. Outside the big three regions, Latin America and the Middle East grow from a lower base, with Brazil and Saudi Arabia pursuing upstream integration that may localize solvent capacity over the next decade.

Competitive Landscape

The Pharmaceutical Solvents market is moderately fragmented. Emerging challengers focus on bio-based solvents and mechanochemistry that eliminates liquids entirely for certain peptides, but capital hurdles and multi-year REACH registrations slow entry. Technology adoption is now a competitive wedge: blockchain inventory tracking and AI-driven demand forecasts cut lead-time variability, a critical advantage as regulators intensify supply-chain scrutiny.

Pharmaceutical Solvents Industry Leaders

BASF

Dow

Eastman Chemical Company

Merck KGaA

Avantor, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Advent introduced two specialized solvent grades, LN (Low Non-volatile) and LCN (Low Non-volatile Chromatography). These innovations aim to tackle a persistent challenge in research and pharmaceutical laboratories: the presence of hidden impurities in solvents that jeopardize analytical precision.

- May 2025: Univar Solutions LLC announced that its Ingredients and Specialties (I+S) from the Univar Solutions division was appointed the preferred distributor for Tedia Company LLC's ("Tedia") high-purity solvents and ultra-high purity (UHP) oligonucleotide and peptide synthesis (ONS) chemicals in the United States and Canada for pharmaceutical and biopharmaceutical applications.

Global Pharmaceutical Solvents Market Report Scope

Pharmaceutical solvents are liquids used to dissolve, suspend, or extract active pharmaceutical ingredients (APIs), crucial for manufacturing, stability, and drug delivery. Common types include water (most common), alcohols (ethanol, IPA), and glycols (propylene glycol), with regulatory guidelines classifying them into three classes based on toxicity.

The Pharmaceutical Solvents market is segmented by type, function, application, and geography. By type, the market is segmented into Alcohols (Ethanol, Isopropanol, Butanol, and More), Glycols (Propylene and Ethylene), Ethers (Diethyl Ether and THF), Esters (Ethyl and Butyl Acetate), Chlorinated Solvents (Methylene Chloride and Chloroform), Aromatic Hydrocarbons (Toluene and Xylene), Ketones (Acetone and MEK), and Other Types (Alkanes, Super-critical Fluids, and Ionic Liquids). By function, the market is segmented into reaction medium, extraction solvent, purification/crystallization, and formulation and blending agent. By application, API Manufacturing, Formulations (Oral, Injectable, and Topical), Drug-Delivery Systems, Biopharmaceutical Production, Analytical and QC Laboratories, and Other Applications (Cleaning, Sterilization, and Packaging). The report also covers the market size and forecasts for pharmaceutical solvents in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Alcohols (Ethanol, Isopropanol, Butanol, etc.) |

| Glycols (Propylene, Ethylene) |

| Ethers (Diethyl Ether, THF) |

| Esters (Ethyl, Butyl Acetate) |

| Chlorinated Solvents (Methylene Chloride, Chloroform) |

| Aromatic Hydrocarbons (Toluene, Xylene) |

| Ketones (Acetone, MEK) |

| Other Types (Alkanes, Super-critical Fluids, Ionic Liquids) |

| Reaction Medium |

| Extraction Solvent |

| Purification/Crystallization |

| Formulation and Blending Agent |

| API Manufacturing |

| Formulations (Oral, Injectable, Topical) |

| Drug-Delivery Systems |

| Biopharmaceutical Production |

| Analytical and QC Laboratories |

| Other Applications (Cleaning, Sterilization, Packaging) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Alcohols (Ethanol, Isopropanol, Butanol, etc.) | |

| Glycols (Propylene, Ethylene) | ||

| Ethers (Diethyl Ether, THF) | ||

| Esters (Ethyl, Butyl Acetate) | ||

| Chlorinated Solvents (Methylene Chloride, Chloroform) | ||

| Aromatic Hydrocarbons (Toluene, Xylene) | ||

| Ketones (Acetone, MEK) | ||

| Other Types (Alkanes, Super-critical Fluids, Ionic Liquids) | ||

| By Function | Reaction Medium | |

| Extraction Solvent | ||

| Purification/Crystallization | ||

| Formulation and Blending Agent | ||

| By Application | API Manufacturing | |

| Formulations (Oral, Injectable, Topical) | ||

| Drug-Delivery Systems | ||

| Biopharmaceutical Production | ||

| Analytical and QC Laboratories | ||

| Other Applications (Cleaning, Sterilization, Packaging) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the pharmaceutical solvents market be by 2031?

The pharmaceutical solvents market size is projected to reach USD 7.65 billion by 2031 from USD 5.96 billion in 2026 at a 5.13% CAGR.

Which solvent category grows fastest?

Ionic liquids, supercritical fluids, and other next-generation solvents are forecast to expand at 5.80% CAGR through 2031.

Why is Asia-Pacific attracting new capacity?

A combination of expanding CDMO infrastructure in China, India, and South Korea and supportive government programs is driving the region’s 6.02% CAGR.

What drives demand in biopharmaceutical production?

Multi-stage chromatography for monoclonal antibodies and cell-and-gene therapies sharply increases the need for ultra-high-purity solvents.